Most Popular

-

1

Ador CEO denies allegations, accuses Hybe of mistreating NewJeans

-

2

Medical reform committee kicks off despite boycott from doctors

-

3

10-man S. Korea lose to Indonesia to miss out on Paris Olympic football qualification

-

4

DP leader says he will meet Yoon without conditions

-

5

Over 9,000 hotline calls made by stalking victims in 2023

-

6

[Hello India] Hyundai Motor vows to boost 'clean mobility' in India

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

-

7

Hybe-Ador feud should have limited effect on Hybe's overall performance: analysts

-

8

Monthly users on local streaming platforms outpace Netflix, Disney+

-

9

US will take steps for three-way engagement on nuclear deterrence with S. Korea, Japan: Campbell

-

10

Second Gimpo civil servant found dead, after apologizing for not finishing work

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

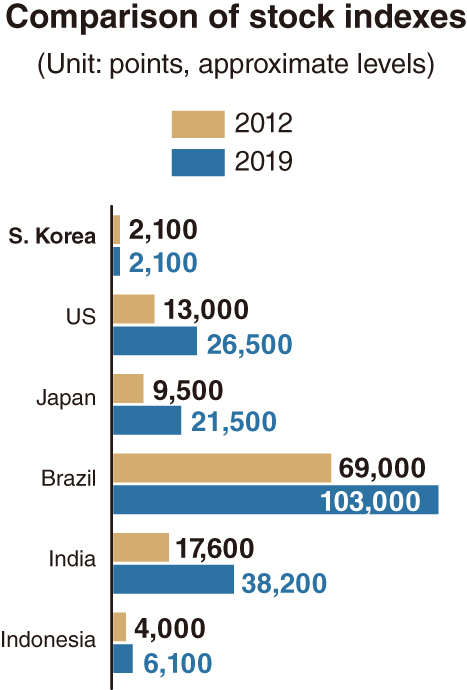

[News Focus] Korean stocks lag behind foreign rivals

By Kim Yon-sePublished : Oct. 13, 2019 - 12:53

They cite favorable external factors involving eased concerns about the trade dispute between the US and China as the prospects of a bilateral compromise grow.

The benchmark Kospi has been swayed by external factors like global financial crisis over the past few years or decades. However, likewise, other major economies also frequently saw their stock markets hit by the sort of negative factors.

Despite fundamentals of Korean equities, data shows that the Kospi made little progress in terms of price growth over the past decade compared to indexes of other major economies.

The Dow Jones industrial average, which was at around 9,500 points about 10 years ago, climbed to trade over 15,000 mark in 2015. The US stock price index is now hovering around 27,000 points, posting about 180 percent growth in a decade.

The Nikkei 225 on the Tokyo Stock Exchange ranged 9,500 mark between 2010 and 2013, hit by the 2008-09 global financial crisis. But the Japanese benchmark index has continued to gain, since then, to exceed 21,000 points this year.

The long-term bullish situation is also seen among some Asian emerging markets.

India’s Sensex index, which stayed around 18,000 in 2013, has recorded more than a 100-percent gain to reach 38,000 points this year. Indonesia also posted 100 percent in gains less than 10 years to surpass the 6,100 mark.

The main index Bovespa of Brazil posted more rapid pace in growth – from the 46,000 mark in 2016 to about 103,000 in 2019.

Over the past decade, Germany’s Dax 30 also showed a surge by about 100 percent to the 12,000 level, while the UK’s FTSE 100 increased on a gradual basis from 4,500-5,000 to break through 7,000 points.

The Kospi’s situation is quite contrast to that of the indexes above. Though some politicians and finance-industry experts had painted rosy pictures that it could surpass the 3,000 mark to approach 4,000 points, the Korean index is currently staying at the level, posted nine or 10 years ago.

If the relatively short-term bullish position to surpass 2,500 points in 2018, when Pyongyang-Washington summit was held, is excluded, the Kospi has been stuck between the 1,800-2,200 boundary since 2011. It has gained de facto zero for a decade.

It is also contrasted to the property market domestically, in which a large portion of apartment prices in Seoul soared 50 to 100 percent in less than five years.

“A core factor for the sluggish capital market vs. a record-breaking spike in the real estate market lies in politics,” said a research analyst in Yeouido, Seoul.

His remarks mean that the nation’s low interest rate era, which has continued since 2014, is not attractive to stock investors, as the local currency lost ground against key currencies such as the dollar, yen and euro.

Though the nation has been successful in boosting the property market via a series of rate cuts in attempt to raise GDP growth rates, the nation simultaneously has aggravated uncertainty over its currency value in the global stage.

The previous Park Geun-hye administration led a construction-oriented stimulus policy, and the incumbent Moon Jae-in administration has yet to normalize interest rates.

South Korea’s base rate, which was 3.25 percent per annum in 2011, has been set at 1.5 percent since July 2019. The Bank of Korea has kept the rate under 2 percent since March 2015.

An analyst refuted the idea, claiming that the stagnant situation in Kospi index is long-standing geopolitical risks on the peninsula.

“The 2018 spike in stock prices, buoyed by peace talks, indicate the great potential of local stocks,” he said.

Meanwhile, many small investors pick financial authorities’ lukewarm stance toward short-sellers.

“Reckless short-selling by local and foreign institutions is still curbing index performance,” said an individual investor.

By Kim Yon-se (kys@heraldcorp.com)